LIDERAGORA.net | El blog de Daniel Sánchez Reina

Un espacio de lectura y reflexión sobre Gestión Empresarial y Liderazgo. Y si quieres todavía más… todos los JUEVES a las 16:20 (GMT+1), en CAPITAL RADIO, mi sección "QUIERO SER UN BUEN JEFE"

POST-COVID19 WORLD (III): Macroeconomics changes

This is the third (and last) of a series of articles about the world that awaits us out there.

The perspectives showed in this article and their intensity will depend very much on how long it takes until a vaccine is found, released and delivered, or until we get immunized at levels of over 60% of population (which is the percentage considered as herd immunity by the WHO).

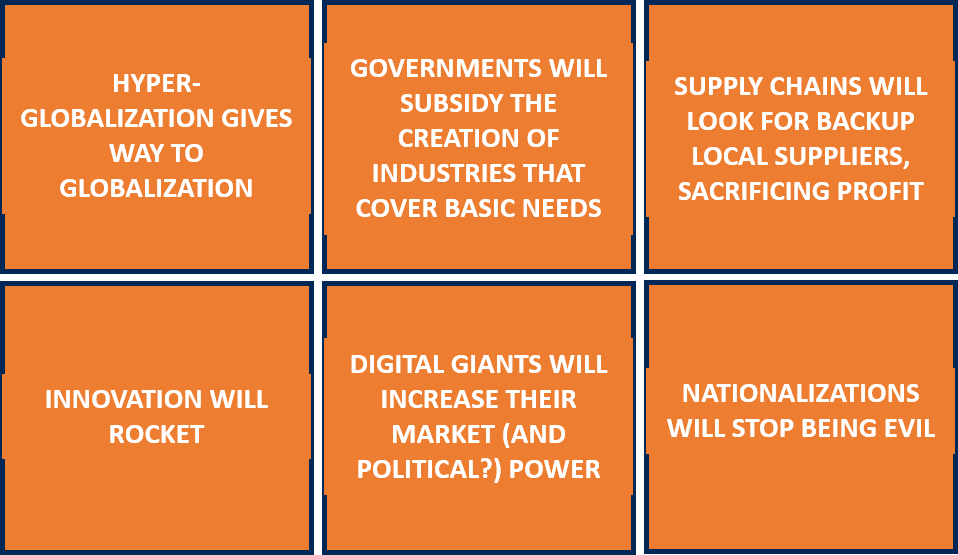

HYPER-GLOBALIZATION GIVES WAY TO GLOBALIZATION

In practical terms we were not living in a globalized world, but in a hyper-globalized one. Economic globalization started at the end of WWII, with the extensive transfer of production capacity from highly developed countries to developing countries, seeking cost reductions and massive workforce. Then it gradually extended also to the movement of capitals, services and people, up until today.

This pandemic will force us to rethink this model. Lockdown measures and the concentration of some basic products (food, hygiene and sanitary) beyond our borders, pose a high risk to the livelihood of countries during pandemics.

There will be a surgical (not a massive) re-localization of production capacity for those basic products, to guarantee supplies withing countries’ borders. In other words, we will transition from the current hyper-globalized world to simply a globalized world, not to a localized one. A localized world is a highly unlikely scenario, not only because it would severely damage profits of nearly all industries in the world, but primarily because the suppliers game is so scattered and highly intertwined in the globe, that self- sufficiency is a chimera.

GOVERNMENTS WILL SUBSIDY THE CREATION OF INDUSTRIES THAT COVER BASIC NEEDS

As a side effect of the previous section, governments will ensure that their countries are self-sufficient as per basic products. Industries like agriculture, lifestock, fishing, hygiene and sanitary materials will be reinforced or even created from scratch in many countries. It is unlikely that those newly created or expanded industries will become the main suppliers for their own countries if that was not the case before the pandemic, but they will gain a significant market share.

Governments will subsidy the creation, renovation and expansion of such local industries, at least to guarantee enough stock and supplies to resist some months of lockdown period.

SUPPLY CHAINS WILL LOOK FOR BACKUP LOCAL SUPPLIERS, SACRIFICING PROFIT

During this pandemic many enterprises found themselves unable to get the goods and raw materials they needed for their sales and manufacturing processes, due to lockdown measures at the supplier country.

Seemingly immediate solution: searching for a second (backup) supplier. But, if you search for it abroad again, it may leave you in the same weak position in the event of a future outbreak of the virus. That is the reason why most enterprises will reach agreements with local suppliers, even though sacrificing cost -hence profit-, quality or service.

But difficulties do not end here. Treating the local backup supplier as a last-resort option or committing just a minimum annual purchases to keep a minimum business relationship, will not develop sufficient loyalty between your supplier and you. In the event of another virus outbreak, you will be the last priority for the backup supplier. You may find yourself coping with the same shortage issues as during this pandemic. Most likely you will have to increase the business volume with the backup supplier, so that it is not a last-resort but another business-as-usual source of goods.

INNOVATION WILL ROCKET

Lockdown measures have split enterprises in two groups: those able to sell their goods and services during the pandemic, and those unable.

Leaving aside those enterprises whose nature of business is physical (e.g. travel and hospitality), there are many who did not overcome the lockdown period in good shape because their business models were not resilient against a pandemic. In anticipation of a future virus outbreak, they will incorporate innovations like digital channels, changes in the mix of portfolios or creation of new products/services to become resilient.

Something similar will apply to national agencies. They will have to increase their digital offer, due to the impossibility of physically attending their offices during lockdowns.

Likewise, social distancing measures will force some industries to find additional ways to attract those customers that otherwise they would lose. High-street retail, travel and hospitality are the main examples of that. Most of those solutions will lie in creating digital sales channels, home-delivery service, or focus on domestic travel and on domestic customers.

DIGITAL GIANTS WILL INCREASE THEIR MARKET (AND POLITICAL?) POWER

Those businesses that decide to create digital sales channels will be smart enough to not reinvent the wheel. They will use the platform ecosystems already in the market (digital giants like Amazon, Google, Apple, Alibaba, Tencent,…) to leverage their huge capabilities in logistics and sales.

That will make those digital giants even more powerful than they are today. It is not an issue from a market perspective, because it is not a transfer of market share from the small platforms to the giants, but an extension of the pie.

The novelty is that those giants are becoming so big and influential that they also have the power to provide some social services that have been traditionally served by governments. Examples: Apple and Google’s agreement to track and trace corona-infected people to identify them and isolate them immediately; or Amazon granting loans to small manufacturers to survive (although this is kind of win-win).

When you have the capacity to provide services that governments should be providing, your political influence increases. The question mark is if and how such political power will be exerted.

NATIONALIZATIONS WILL STOP BEING EVIL

In liberal democracies the word «nationalization» of enterprises has always been considered evil because it attempted against the fundamental roots of capitalism. However, after this pandemic, many governments will consider to participate as shareholders in some industries that are strategic to preserve livelihood during times of lockdown and sanitary crises.

Equally, some economic sectors not related to livelihood but very relevant to GDP (directly or indirectly through auxiliary sectors), like airlines, will need either a M&A (Merges and Acquisitions) to survive, or bailouts from governments.

in the case of bailouts, and in order to preserve the essence of capitalism, governments will demand entering the companies’ shareholding temporarily -contrary to what happened with banks bailout during the subprime depression in 2008, to guarantee that the money goes back to the State coffers after recovery-. It can be permanent in the case of strategic companies for livelihood. Regardless of temporary or permanent, it will pose a competition issue with the rest of companies of the same industry which have not been bailed out. It will be thoroughly tackled by strict and stringent rules to impede governments to inject more than just the minimum amount of money necessary to start operating and no more injections moving forward.

The future may be a negative self-fulfilling prophecy or a set of opportunities to build a better world. Either of those two options may be true. It’s in our hands.

If you missed them, find here below the other two articles of this series:

I wish you the best.

Daniel Sánchez Reina

Si quieres seguir mi blog, a la derecha de la pantalla (o abajo, según el dispositivo) encontrarás el botón.

Autor de El mentor (Ed. Almuzara).

Co-autor de El dilema del directivo (LID Editorial).

Escucha todos mis podcasts de Capital Radio.

Publicaciones Populares

EL MENTOR

EL DILEMA DEL DIRECTIVO

QUIERO SER UN BUEN JEFE (podcasts)

EL MENTOR

EL DILEMA DEL DIRECTIVO